SPECIAL: SCOTTISH INDEPENDENCE IMPACT

10th Sep 2014

WE’VE ALL HEARD THE ARGUMENTS BOTH FOR AND AGAINST SCOTTISH INDEPENDENCE, YET THERE SEEMS TO BE SILENCE IN THE MEDIA ON HOW THE REFERENDUM WILL AFFECT BUSINESS IN SCOTLAND AND THE UK AFTER THE 300 YEAR OLD UNION HAS BEEN DISSOLVED.

Not too long ago in August, over 130 CEOs of major Scottish businesses such as Weir Group, BP, BHP Billiton, Standard Life and RBS came together to plead that the “business case” for Scottish independence had not been made. These businesses represented at least 50,000 jobs in Scotland with some businesses threatening to move their operations to England.

However, since then the CEO of Stagecoach, CEO of Scottish Mortgage Investment Trust and others prominent members of the Scottish community have voiced their support to separate, claiming that;

“FOR TOO LONG ECONOMIC POLICIES HAVE NOT FAVOURED SCOTLAND NOR ENCOURAGED THE SME SECTOR”

The rest of the UK has only just been ‘rudely awoken’ to the fact that independence could now very much be a possibility with polls showing the referendum will now be ‘too close to call’.

SNAPSHOT OF ISSUES THAT WOULD EFFECT UK BUSINESS

CURRENCY

Both the Pro-independence and Pro-Union sides have expressed their disputed views of what the currency of the newly formed Scotland would be.

If there were to be no currency union – which has largely been ruled out by the UK government – it is likely that borrowing costs are going to increase.

If there is a new currency or the joining of the Euro, this would result in uncertainty and therefore little trust in the newly formed Scottish economy. The knock on effect would be much more substantial.

Since the financial crisis, the close relationship between the creditworthiness of sovereigns and their domestic banking systems has meant that a one-percentage-point rise in funding costs for the sovereign can result in bank funding costs increasing by between 0.15 and 0.2 percentage points.

For SMEs – typically more dependent on bank finance for business loans and mortgages – this will likely have consequences for their cost of borrowing. Again having a knock on effect to the day to day operations of business and also the businesses ability to innovate and expand operations in the future.

LOWER CORPORATION TAX RATES

The proposals put forth by the SNP government have suggested that they could and would lower Corporation tax rates to attract business to the new country which could entice new engineering and manufacturing opportunities north of the border.

However, the effectiveness tocut CT rates to increase business investment, wildly vary from industry to industry. There is not enough clear evidence to suggest that a cut in CT would have a direct correlation to a growth in business output in Scotland.

TRADE

One of the only certain outcomes of the referendum is that there will be a new international border if there is a Yes vote, and previous evidence from the international community shows that introducing a border hinders trade.

Transactional costs, separate currencies, administrative procedures and different regulations can effect a company’s ability to trade internationally with a foreign country.

– SCOTLAND’S TRADE WITH THE REST OF THE UK DWARFS ITS TRADE WITH OTHER COUNTRIES. IN 2012

NON-OIL EXPORTS TO THE REST OF THE UK STOOD AT £48 BILLION

– 61% OF THIS TRADE WERE MANUFACTURED GOODS EQUALLING £29.28 BILLION

– SCOTLAND’S IMPORTS FROM THE REST OF THE UK TOTALLED £59 BILLION IN 2012

– 58% OF THIS TRADE WAS CATEGORISED AS MANUFACTURED GOODS EQUATING TO £34.22 BILLION

Similarly, Scotland exported £1.9 billion of goods and services in 2012 from the Machinery & equipment sector, while at the same time importing £1.7 billion of products from the same sector. (Weir Group – 2014)

This type of observation supports a more nuanced view of the drivers to trade. This emphasises the impact of economies of scale, and the increasing returns they offer to larger production units, as a force behind the concentration of certain industries and their supply chains in particular locations. The size of the domestic market and transport costs associated with the product are important considerations and are key areas to be effected by independence.

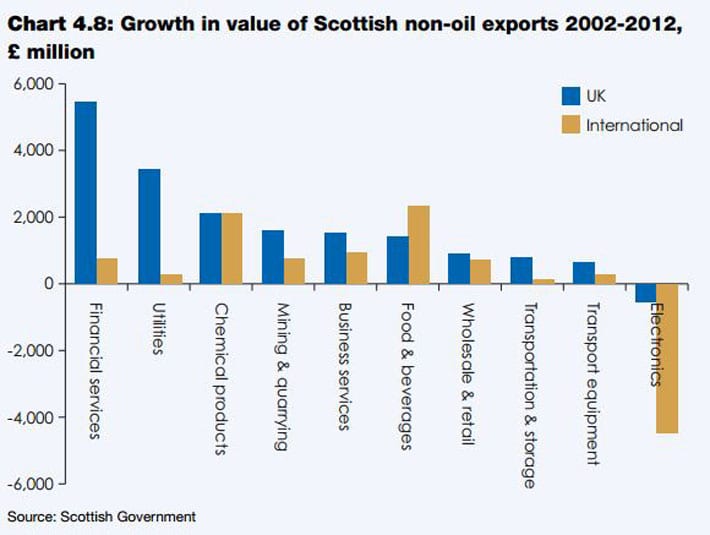

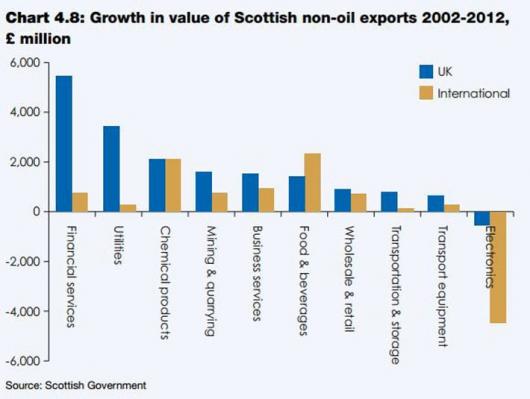

If we look specifically at the manufacturing industry of Scotland and the biggest contributors to growth in the value of Scottish non-oil exports from the rest of the UK;

Chemical Products accounted for £2billion worth of growth within Scotland from 2002 to 2012, utilities accounted for £3.8billion (including water and wastewater) and food & beverage accounted for £1.6 billion worth of growth.

This growth was sustained because there were no barriers to trade, after independence there is a possibility that we would not see growth like this again from the rest of the UK on Scottish trade.

IMPACT TO THE REST OF THE UK

There has been a long stated national aim to rebalance the UK economy by pushing for UK business to manufacture and export more, tilting our economy away from services. Independence would hinder the UK’s ability to do such a thing.

Despite the efforts of recent governments, the trade deficit has widened to near record levels. Oil and chemicals – two particularly strong sectors in Scotland – have been two segments to constantly ‘buck the trend’ (ONS 2013) providing more exports than imports.

Manufacturing has not fully recovered to pre-recession levels with imports rising more than twice as fast as exports.

Lee Hopley from the EEF argued that UK manufacturers are more concerned with the domestic market than exporting, considering the state of the Eurozone economies and geo-political situations.

“Independence would create a new export market for the rest of the UK as it currently sells more goods and services to Scotland than it buys. Independence might also deliver Scotland’s £1.4bn financial services industry to London, although that will hardly help the rebalancing effort” (theengineer.co.uk)

However, the loss of the oil and gas industry (currently a major factor in rising exports) is likely to have a serious impact on the rest of the UK’s trade imbalance. The BBC calculates that it would have increased last year’s deficit of 4.4 per cent of GDP to nearly 7 per cent.

TO CONCLUDE, THESE ARE THE MAIN FACTORS THAT WOULD EFFECT BUSINESS AND TRADE AFTER INDEPENDENCE;

– STABILITY AND CREDIBILITY OF THE NEW CURRENCY ARRANGEMENTS.

– ATTRACTIVENESS OF POST-INDEPENDENCE SCOTLAND AS A LOCATION FOR SECTOR-LEADING FIRMS LIKELY TO BE ENGAGED IN CROSS-BORDER TRADE.

– THE NATURE OF THE BORDER BETWEEN SCOTLAND AND THE REST OF THE UK.

– THE REACTION OF BUYERS (ON BOTH SIDES OF THE BORDER) TO THE CREATION OF A NEW ECONOMIC BORDER IN TERMS OF:

• TRADE FLOWS FOR FINAL PRODUCTS AND THE DEGREE OF HOME-COUNTRY PREFERENCE FOR LESS COMMONLY INTERNATIONALLY TRADED PRODUCTS, SUCH AS SOME AREAS OF SERVICES, INCLUDING FINANCIAL SERVICES;

• THE PURCHASING PREFERENCES OF BUYERS IN CROSS-UK AND MULTINATIONAL SUPPLY CHAINS; AND

• THE DEGREE OF COOPERATION/JOINT PURCHASING BY PUBLIC SECTOR PURCHASERS.

– SUCCESS OF AN INDEPENDENT SCOTLAND’S EXPORT PROMOTION INITIATIVES RELATIVE TO THOSE CURRENTLY UNDERTAKEN FOR SCOTTISH-BASED BUSINESSES BY UK AND SCOTTISH AGENCIES

BUT WHICHEVER WAY THE VOTE GOES ON THURSDAY 18TH OF SEPTEMBER, IT IS MOST LIKELY THAT THE TWO ECONOMIES WOULD REMAIN HIGHLY INTEGRATED. BUSINESSES WOULD CONTINUE TO TRADE AND OPERATE ACROSS THE BORDER AND FAMILIES WOULD CONTINUE TO VISIT ONE ANOTHER.